NVIDIA: The Economic-Profit Burden of an AI Bottleneck

A RiskModels.app visual case study in market-implied expectations.

Conrad Gann · Blue Water Macro Corp / RiskModels.org · conrad@bwmacro.com · Working paper · July 2026

Methodology demonstration of the RiskModels.app economic-profit framework. Not investment advice, a recommendation to buy or sell any security, or a personalized valuation opinion. Ratings and scenario weights classify market-implied assumptions — not buy/sell/hold calls.

Abstract

NVIDIA sits at the center of the AI infrastructure buildout: extraordinary free cash flow, scarcity-enhanced margins, and a powerful software/systems stack. Using live RiskModels.app fundamentals, cost of capital, and risk structure — plus SEC filing anchors for revenue and balance-sheet dollars — we translate market capitalization into a required future economic-profit path.

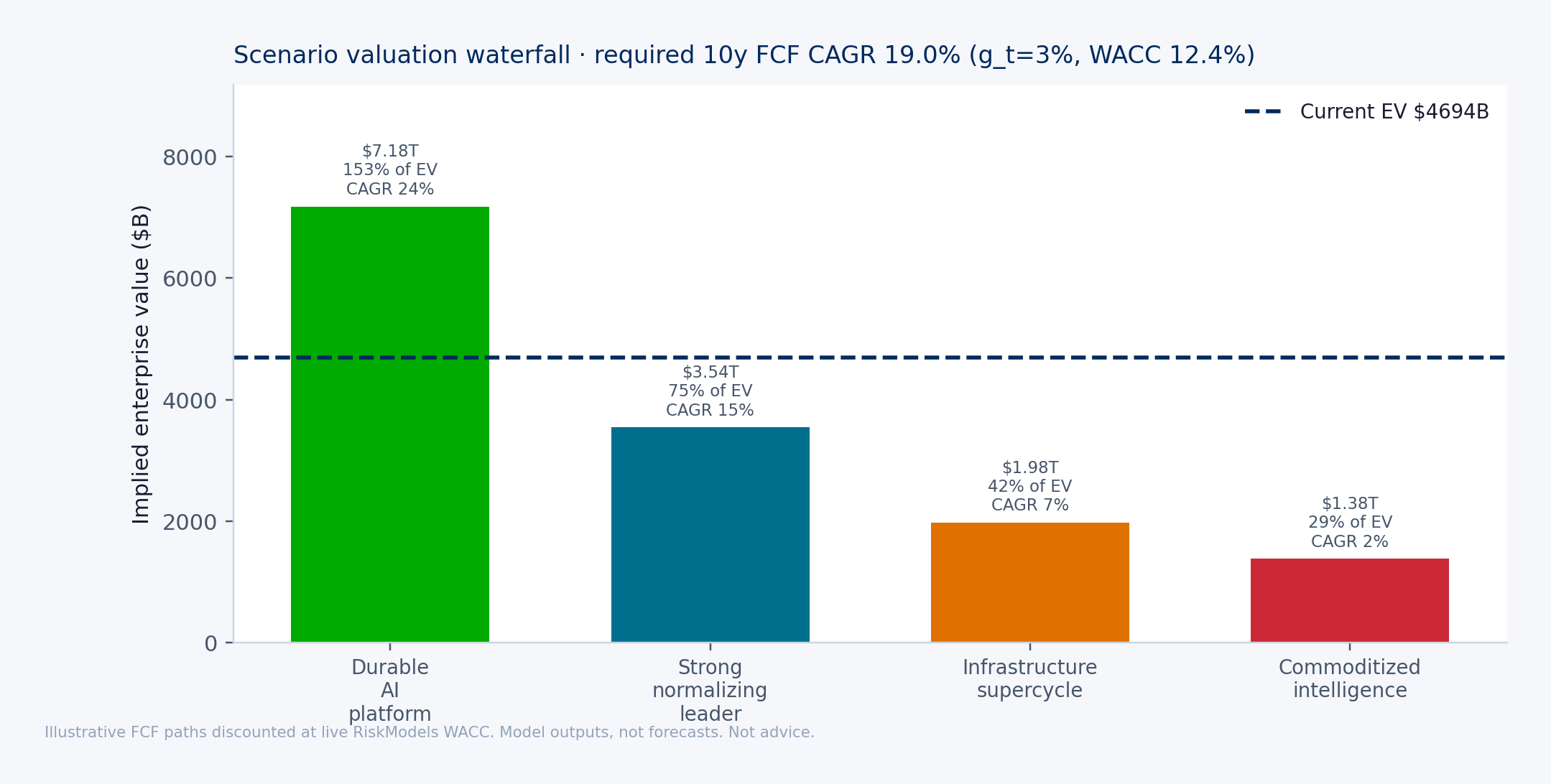

As of the model date in Appendix A, book equity is only a few percent of market cap; capitalizing current economic profit at the cost of equity covers roughly one-third of the present value of future residual income. The remainder is growth-dependent. A reverse DCF at the live WACC implies a high teens required 10-year FCF CAGR under base terminal growth. In the illustrative scenario set, only the durable-AI-platform path clears today’s enterprise value. If the other three scenarios are equally weighted, current EV requires roughly a 50% weight on the durable-platform case.

That is an economic-profit burden statement, not a stock call.

Keywords. economic profit · reverse DCF · residual income · AI infrastructure · bottleneck economics · RiskModels. JEL: G12, G32.

Contents. (1) The question · (2) Risk anatomy (Stock Deep Dive) · (3) Cash-flow step-change · (4) Economic profit · (5) Value bridge · (6) Reverse DCF & scenarios · (7) Industry structure · (8) Peer screen · (9) Implied scenario weights · (10) Burden rating · Appendix A–B.

Key findings & reading guide

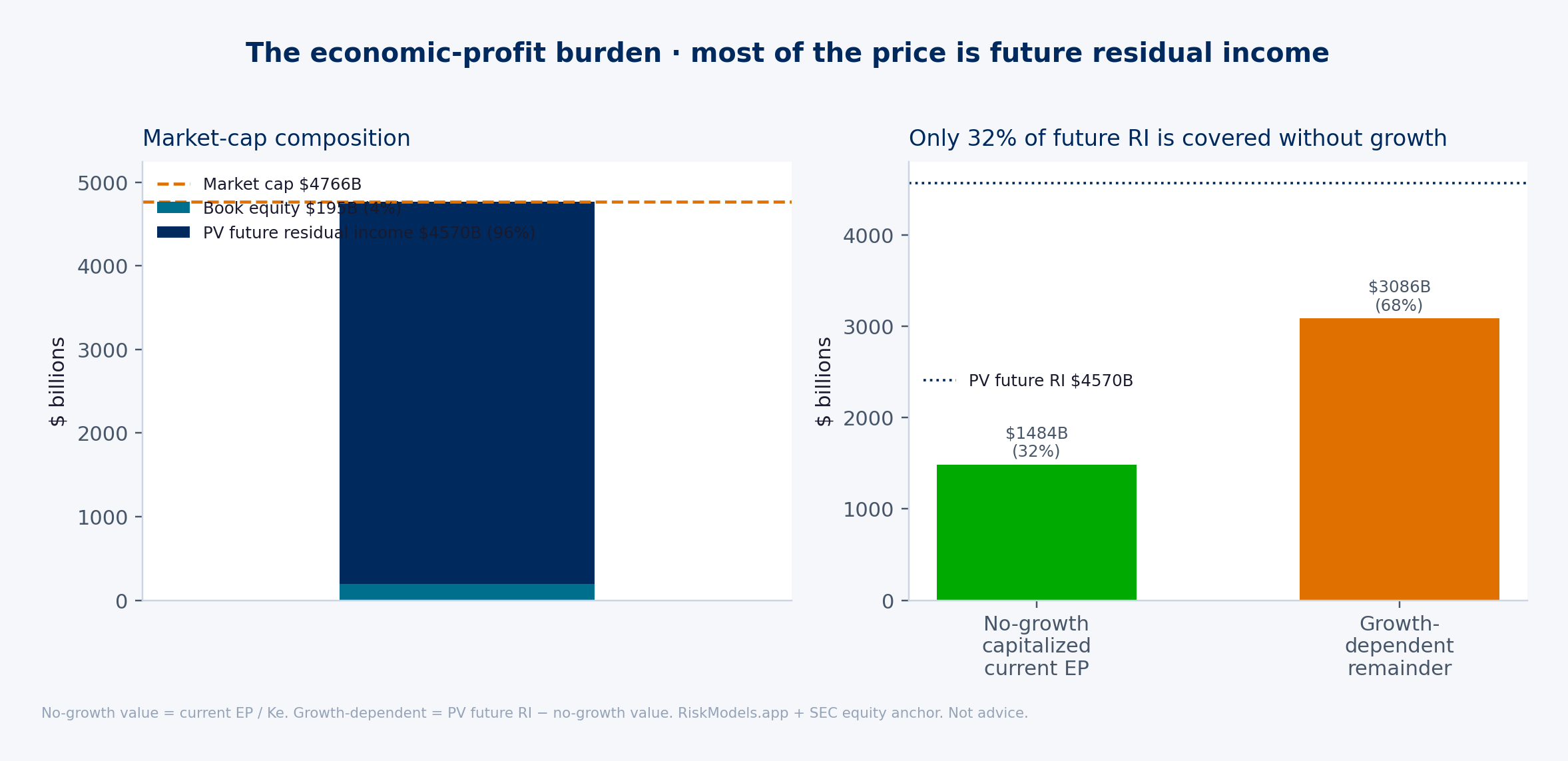

- Book vs growth. Book equity is ~4% of market cap; ~96% is the PV of expected future residual income. Capitalizing current EP at Ke covers only ~33% of that PV — the rest is growth-dependent.

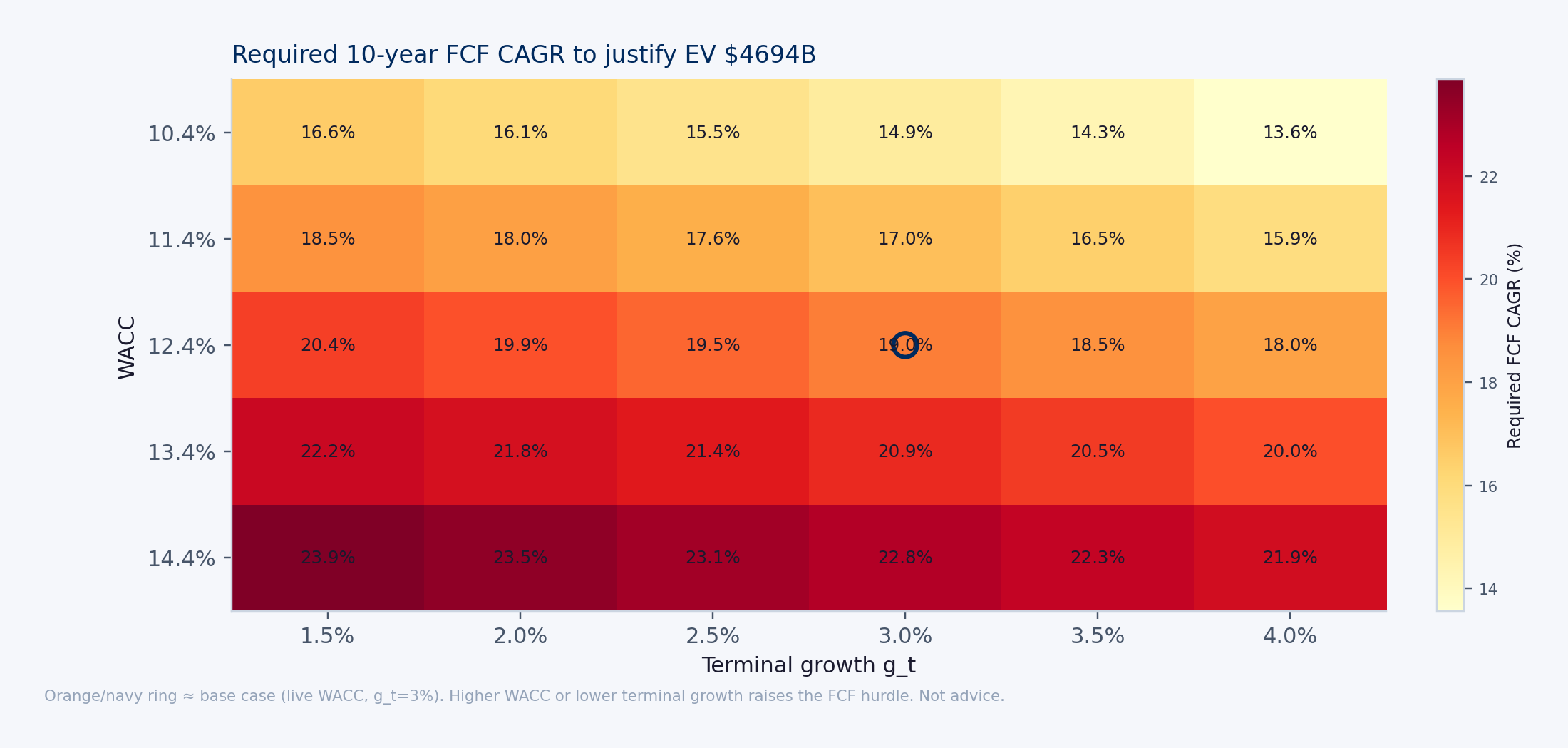

- The hurdle. Required 10-year FCF CAGR at live WACC / gt=3% is ~19% (Appendix A). Only the durable-AI-platform path clears today’s EV in the illustrative scenario set.

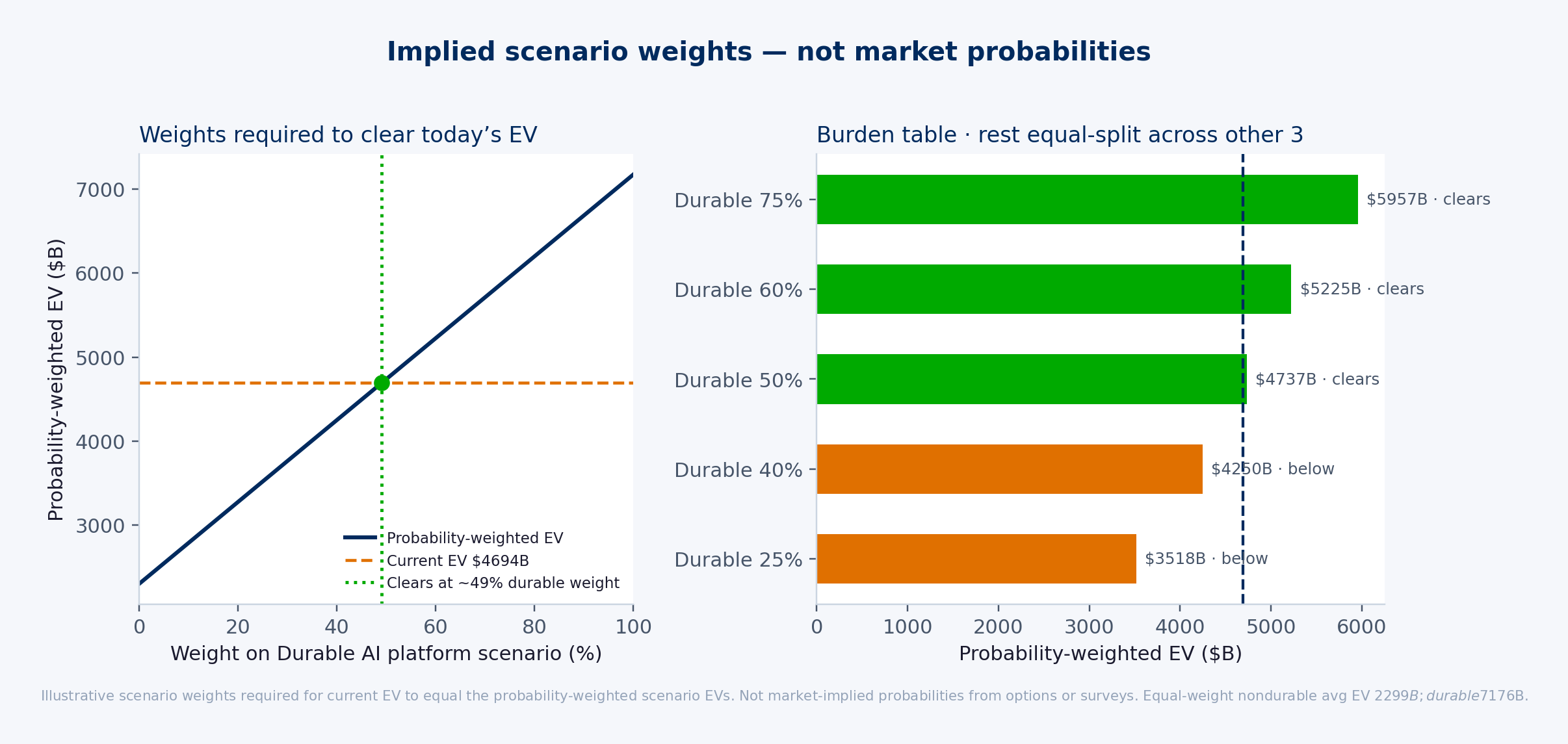

- The weight. With the other three scenarios equal-weighted, current EV requires ~49% weight on the durable-platform case — a required-weight statement, not a market probability.

- Risk anatomy first. Institutional Deep Dive panels show cumulative factor attribution and σ-scaled peer DNA before the EP math — residual share is risk structure, not valuation duration by itself.

- Language. Prefer high market-implied economic-profit burden. Avoid overvalued / sell / short.

Exact live figures refresh from the Appendix B endpoints and print in Appendix A.

1. The question

What must be true for today’s market capitalization to be justified?

For any large-growth company the valuation problem reduces to free cash flow today, growth, reinvestment, duration of returns above the cost of capital, and terminal assumptions. For NVIDIA the sharper form is:

Can a hardware-centered AI infrastructure bottleneck sustain enough economic profit — for long enough — to support a multi-trillion-dollar capitalization?

NVIDIA looks more like a bottleneck profit machine than a classic reinvestment compounder: high FCF and margins, but growth constrained by external capacity (TSMC, packaging, HBM, power) and customer capex. That does not make the business weak. It makes the valuation more dependent on bottleneck duration.

| Type | Description | Valuation support |

|---|---|---|

| Reinvestment compounder | Redeploys retained cash internally at high incremental returns | Multiple supported by reinvestment runway |

| Bottleneck profit machine | Converts a scarce industry position into high margins and FCF | Multiple supported only if bottleneck duration is long |

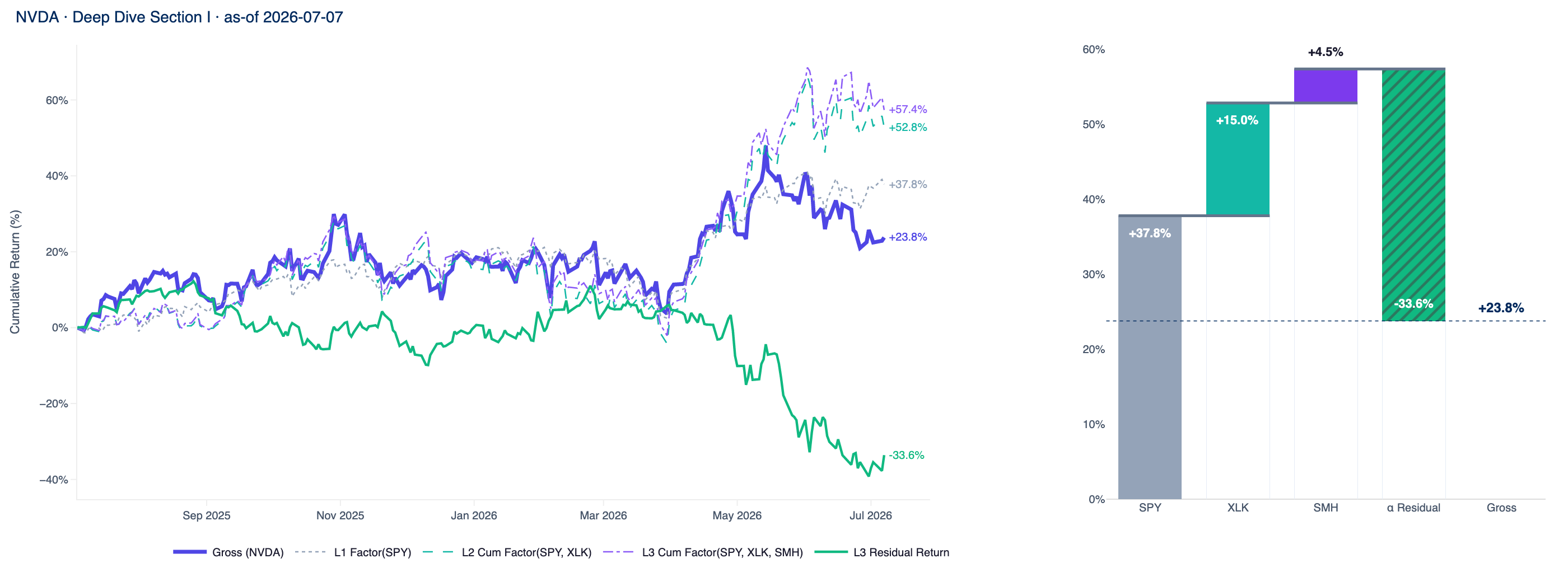

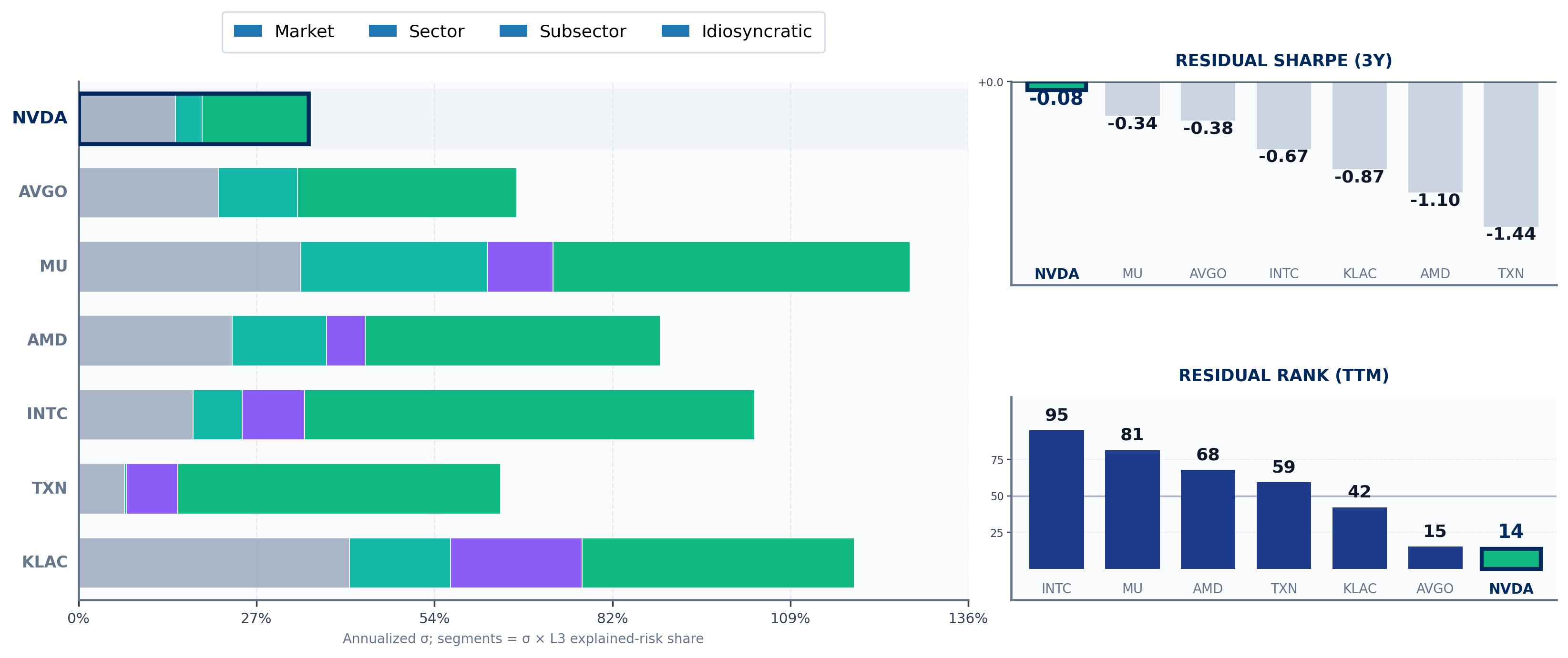

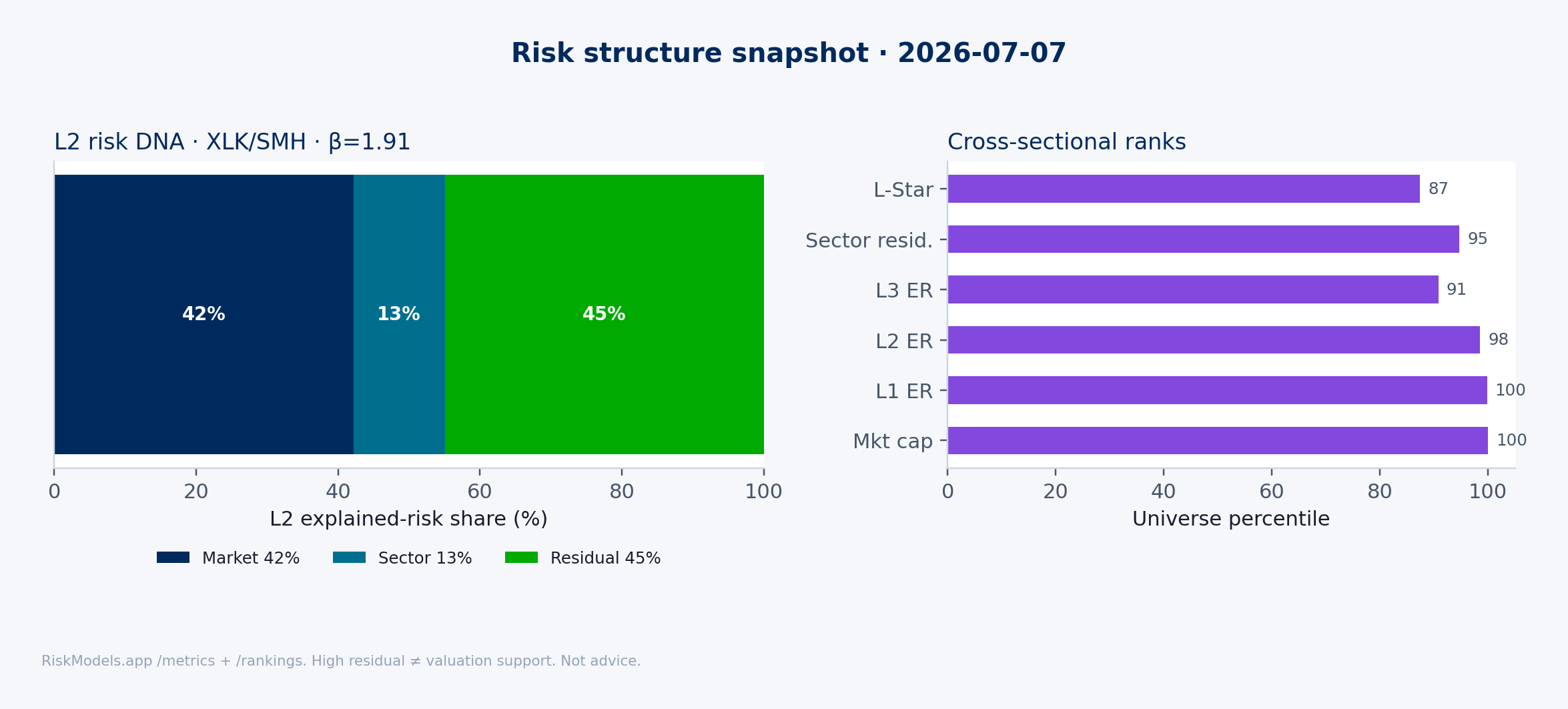

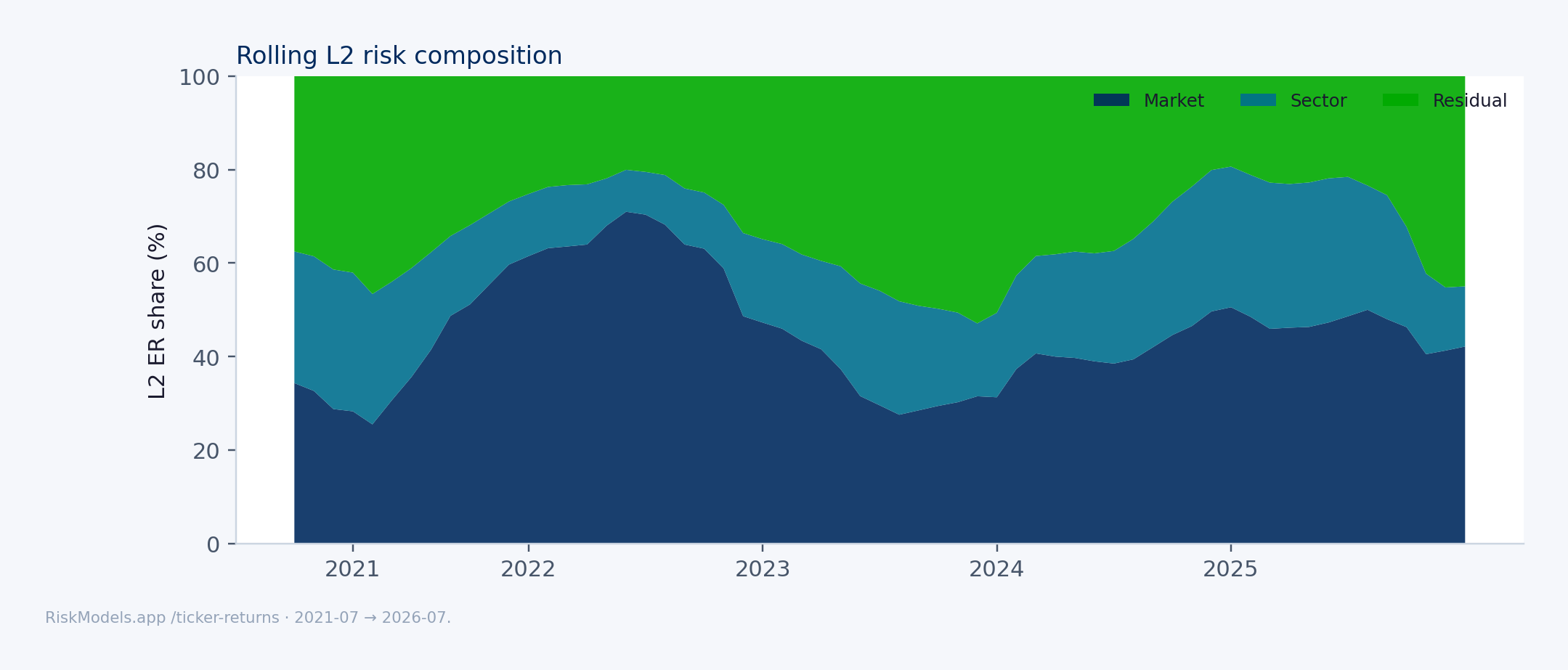

2. Risk anatomy: Stock Deep Dive

Before the economic-profit math, the institutional Stock Deep Dive shows how NVIDIA’s return was earned and how its risk DNA compares to subsector peers. These panels are generated from RiskModels’ institutional Stock Deep Dive workflow, using the same risk, return, and peer surfaces available through the API. DD as-of date is on each chart title; EP model as-of is in Appendix A (they can differ by a day).

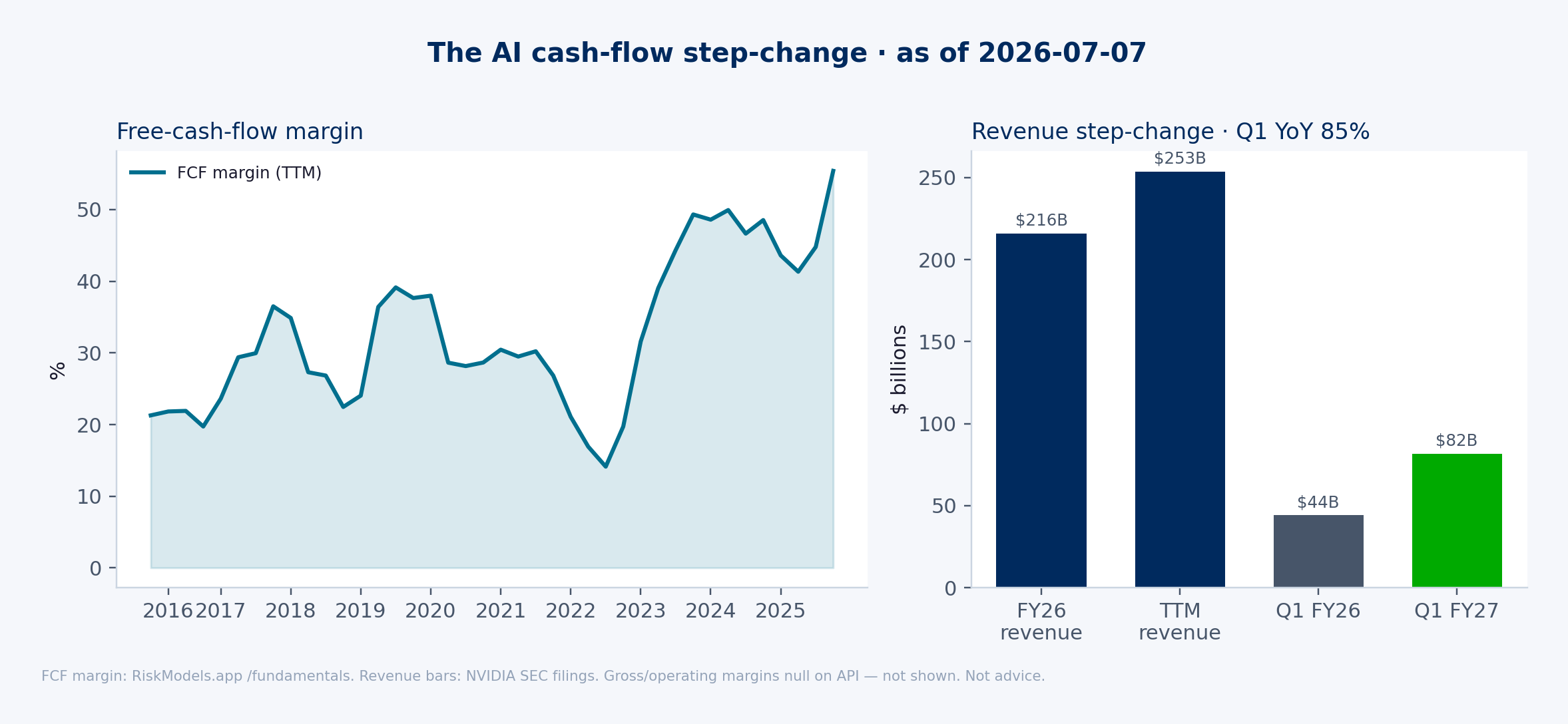

3. The cash-flow step-change

Before asking what the price requires, show the operating step-change. RiskModels exposes TTM FCF margin on the fundamentals history; revenue levels are SEC-cited anchors in the model script (the API does not currently ship raw income-statement dollar lines or gross/operating margins).

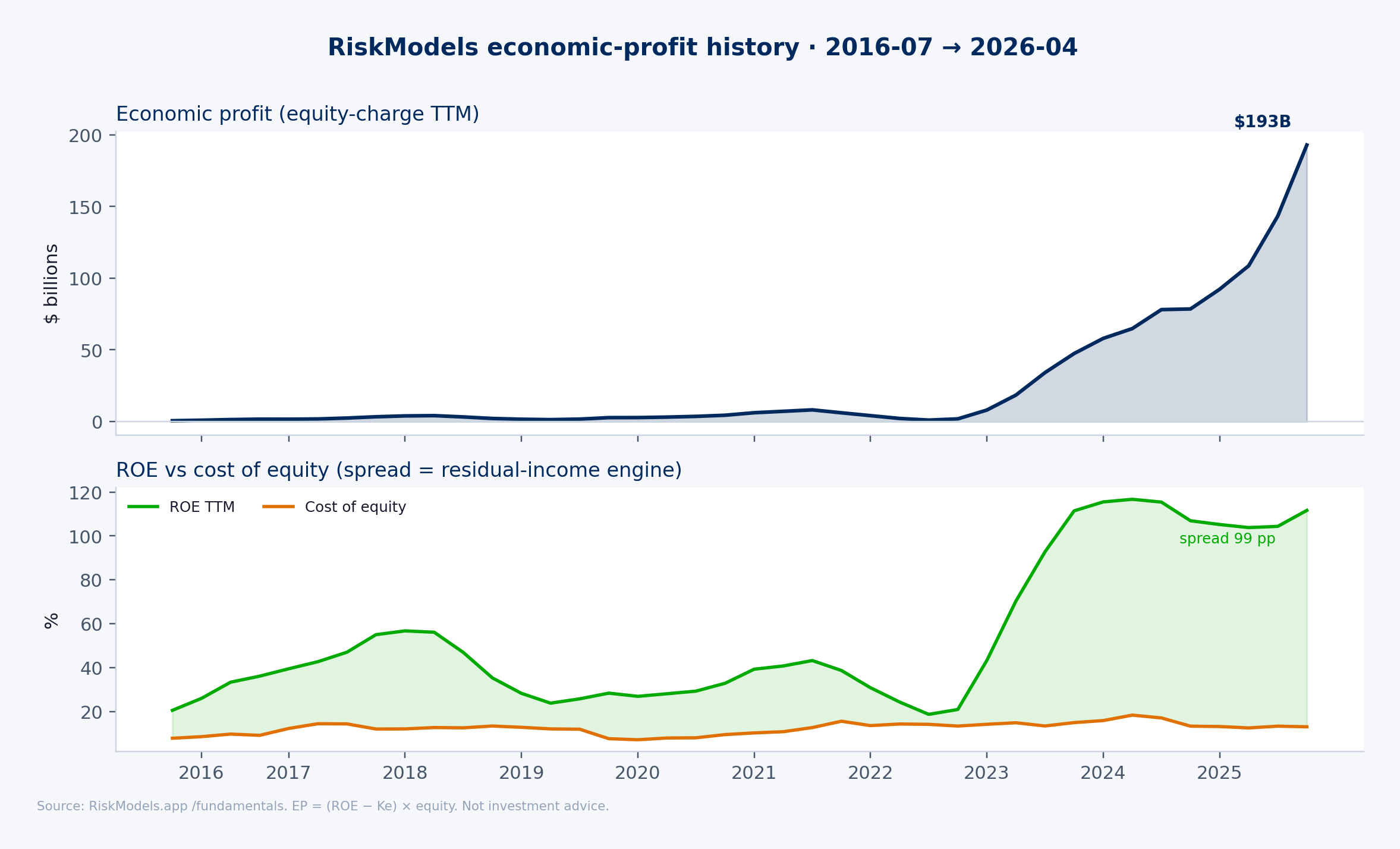

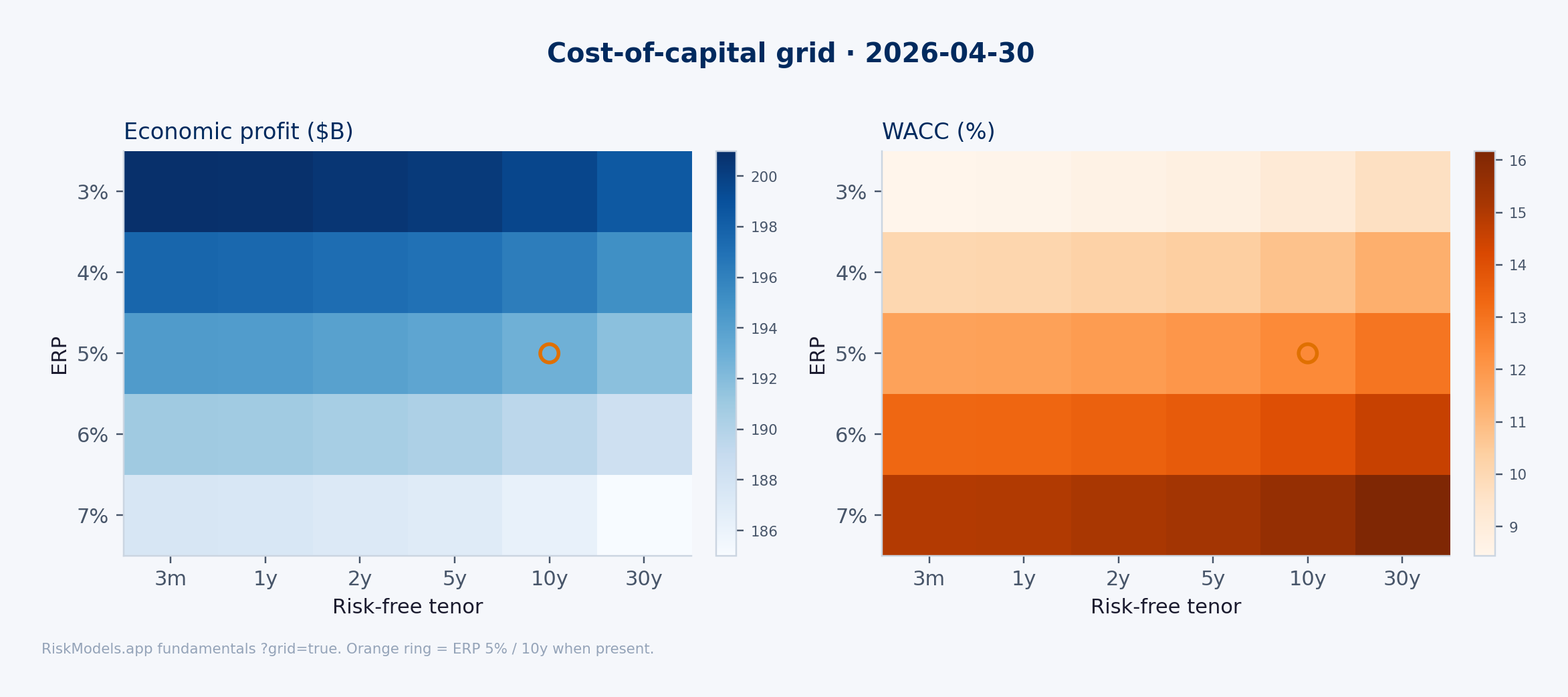

4. Economic profit and the cost-of-capital spread

The RiskModels-native exhibit is equity-charge economic profit and the ROE − Ke spread — the residual-income engine.

5. The value bridge

Most of the market capitalization is not book equity. It is the present value of expected future residual income. Capitalizing current economic profit at Ke (no growth) covers only a minority of that PV; the rest is growth-dependent.

6. Reverse DCF and scenario waterfall

Discount current TTM FCF under illustrative growth paths at the live RiskModels WACC. Compare implied enterprise values to today’s EV. The base-case required 10-year FCF CAGR (terminal growth 3%) is reported in Appendix A and on the chart title.

Robustness: the required FCF CAGR is not a single cherry-picked number. It moves with WACC and terminal growth.

7. Industry structure

Hardware bottlenecks are not interchangeable. Consumer-brand analogies (networks, standards, workflow lock-in) matter less here than physical and capex economics.

| Analogy | Lesson for NVIDIA |

|---|---|

| ASML | Durable when the firm owns a near-irreplaceable physical choke point (EUV). NVIDIA sits atop choke points owned by others. |

| TSMC | Durable but capital-heavy; can reinvest directly into the bottleneck. NVIDIA’s asset-light FCF is attractive because others carry capex — and dependent on their decisions. |

| Cisco | Real infrastructure boom; stock can still disappoint if temporary capex economics are capitalized as permanent. |

| Intel | Architecture shifts can erode even deep hardware moats. |

ASML vs NVIDIA. ASML’s bottleneck is the tool itself. NVIDIA’s current scarcity is a system scarcity — GPUs plus networking plus software — built on wafer, HBM, and packaging capacity it does not own. That is still a powerful position. It is not the same as owning EUV.

Training vs inference. Training rewards flexibility, cluster reliability, and developer familiarity — NVIDIA’s strongest ground. Inference is cost-per-token and utilization: more open to custom silicon once workloads stabilize. The durable-platform scenario needs the stack to remain embedded in both; the supercycle / commoditization scenarios are mostly an inference-and-budget story.

Buyer power. The largest customers have every incentive to dual-source and design ASICs. A high economic-profit burden rating is partly a statement about how long that tension can stay favorable to the supplier.

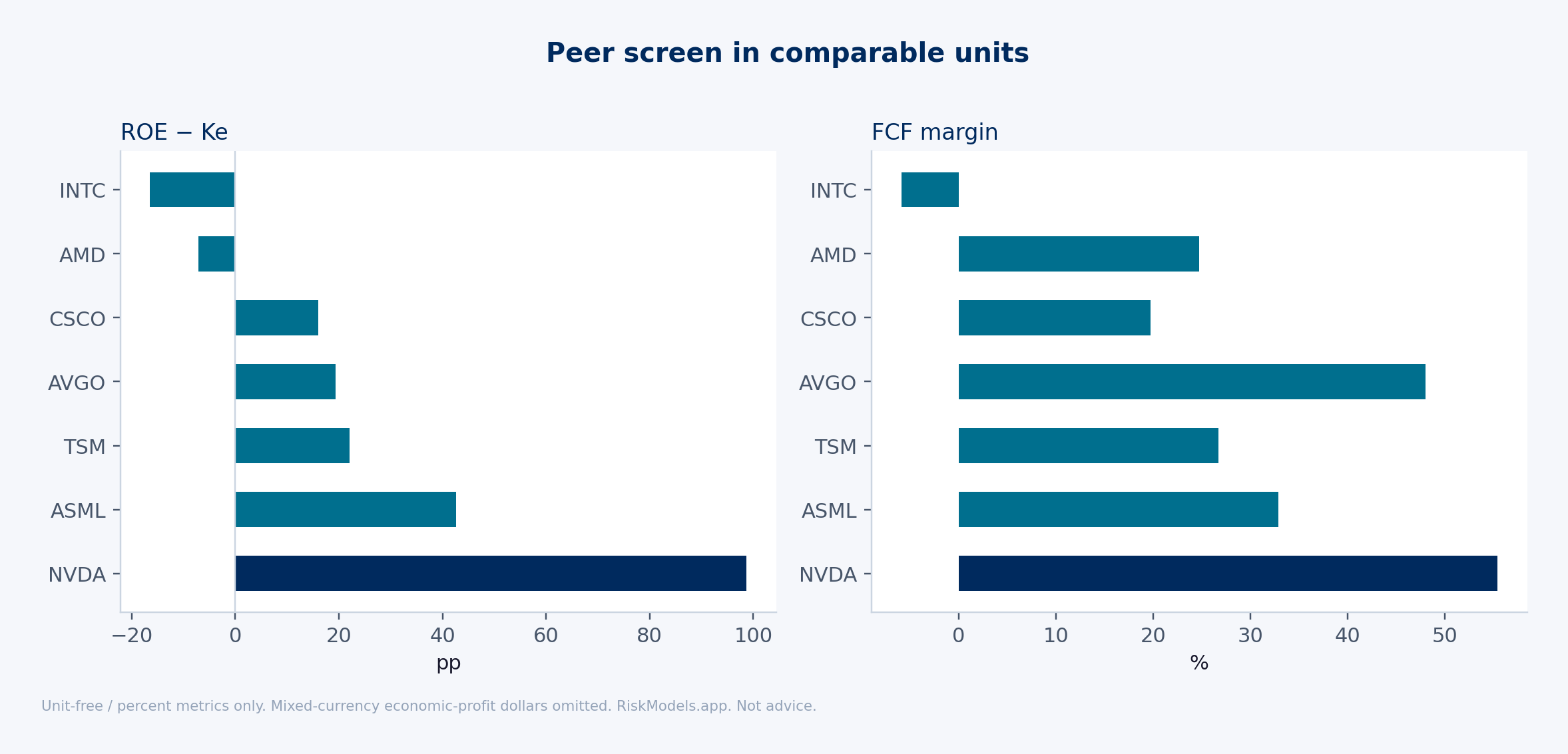

8. Peer screen

Peer economic-profit dollars in EUR/TWD are not USD-comparable. The screen below uses unit-free or %-based metrics only.

9. The probability lens

Do not read the next exhibit as “the market’s actual probabilities.” Options markets and surveys are not used here.

Given four illustrative scenario EVs, ask: what scenario weights are required for the probability-weighted EV to equal today’s EV?

With the three non-durable scenarios equal-weighted, their average EV sits well below current EV. Mixing that average with the durable-platform EV implies a durable-platform weight on the order of ~50% to clear (exact figure in Appendix A).

| Durable AI platform weight | Rest equal-split among other 3 | vs current EV |

|---|---|---|

| 25% | Equal split | Below |

| 40% | Equal split | Below |

| ~50% | Equal split | Near / clears (see live run) |

| 60%+ | Equal split | Above |

Allocator question: Do you believe the durable-platform scenario deserves a ~50%+ weight — that NVIDIA becomes a durable AI infrastructure standard, not merely a strong cyclical leader?

10. Burden rating and “what must be true”

| Output | Classification |

|---|---|

| Economic Profit Burden | High, bordering on extreme — long duration of excess EP embedded in price |

| Reinvestment constraint | High — growth tied to external capacity and customer capex |

| Margin durability risk | Elevated — scarcity-enhanced margins may normalize |

| Inference substitution | Material — custom silicon / cost-sensitive inference |

| Terminal multiple fragility | High — large share of value is terminal / duration |

What must be true (summary)

| Must be true… | Or else… |

|---|---|

| Bottleneck economics persist for a long duration | Growth-dependent RI collapses toward no-growth cover |

| FCF compounds at a high teens+ CAGR for a decade (base WACC / gt) | Reverse DCF misses current EV |

| Durable-platform-like outcomes carry substantial probability weight | Equal-weight cyclical / commoditized paths under-clear EV |

| Training + premium inference remain NVIDIA-heavy enough | Scenario mix shifts toward supercycle / commoditization |

| Terminal assumptions stay premium | Multiple compression dominates even if the business stays strong |

Language to use: high market-implied economic-profit burden. Language to avoid: overvalued / sell / short.

11. Product takeaway

RiskModels.app translates market value into required future economic profit. It connects fundamentals, cost of capital, risk structure, free cash flow, and scenario design so the embedded assumptions are visible.

The objective is not a single fair-value call. The objective is to make the burden measurable.

The same framework can be applied across mega-cap technology, semiconductor supply chains, infrastructure beneficiaries, and other high-expectation equities. The output is not a price target; it is a structured view of the assumptions the market is already underwriting.

User question: What must be true for today’s market capitalization to be justified?

Model answer: current value, FCF, EP, WACC, value bridge, required FCF path, scenario EVs, and the scenario weights that clear the price — with an explicit burden rating, not a recommendation.

Appendix A. Live model snapshot

Computed from RiskModels.app API pulls. Filing dollar anchors are SEC-cited constants; risk, WACC, and economic profit come from the endpoints below. The numeric dump at the end of this PDF refreshes with those same calls.

Appendix B. Method notes

- Economic profit (RiskModels): equity-charge residual income = (ROE − cost of equity) × book equity.

- Value bridge: PV of future residual income = market capitalization − book equity. No-growth cover = current economic profit ÷ cost of equity.

- Reverse DCF: 10-year FCF path plus Gordon terminal growth, discounted at live WACC; solve for the FCF CAGR that matches current enterprise value.

- Scenarios: fixed illustrative FCF-growth and terminal-growth pairs — not forecasts.

- Implied scenario weight: solve for p where p × durable-platform EV + (1 − p) × average EV of the other scenarios = current EV. Not option-implied or survey probabilities.

- Peers: ROE − Ke and FCF margin only (unit-free / percent). Mixed-currency economic-profit dollars are not charted.

- Deep Dive panels: institutional Stock Deep Dive charts from the same RiskModels risk / returns / peer surfaces used on riskmodels.app (cumulative factor attribution + σ-scaled peer DNA + residual Sharpe/rank). Internally rendered via

bwmacro.snapshots.stock.stock_deep_dive(same path as productionnvda_dd_latest).

Reproduce this analysis (API)

The curl / SDK block below is the customer-facing reproduce path. Get a key at riskmodels.app/get-key. Base URL: https://riskmodels.app/api. OpenAPI: riskmodels.app/openapi.json.

export RISKMODELS_API_KEY=rm_... # from https://riskmodels.app/get-key

# Latest risk snapshot — betas, vol, L1–L3 explained-risk shares, hedge ratios, market cap

curl -sH "Authorization: Bearer $RISKMODELS_API_KEY" \

"https://riskmodels.app/api/metrics/NVDA"

# Cross-sectional universe ranks

curl -sH "Authorization: Bearer $RISKMODELS_API_KEY" \

"https://riskmodels.app/api/rankings/NVDA"

# Daily returns + L3 explained-risk / hedge-ratio history (Deep Dive Section I)

curl -sH "Authorization: Bearer $RISKMODELS_API_KEY" \

"https://riskmodels.app/api/ticker-returns?ticker=NVDA&years=3"

# PIT fundamentals — ROE, FCF margin, Ke, WACC, economic_profit (+ optional WACC grid)

curl -sH "Authorization: Bearer $RISKMODELS_API_KEY" \

"https://riskmodels.app/api/fundamentals/NVDA?periods=40&erp=0.05&tax_rate=0.21&grid=true"

# Peer screen — same /metrics call per ticker (unit-free fields only in the paper)

curl -sH "Authorization: Bearer $RISKMODELS_API_KEY" \

"https://riskmodels.app/api/metrics/AVGO"

Python SDK equivalent (pip install riskmodels-py):

from riskmodels import RiskModelsClient

client = RiskModelsClient.from_env()

m = client.get_metrics("NVDA")

f = client.get_fundamentals("NVDA", periods=40, erp=0.05, tax_rate=0.21)

hist = client.get_ticker_returns("NVDA", years=3)